The Ultimate Guide to Travel Banking [How to Get the Best Exchange Rate and More]

Whether you’re planning on traveling long or short term, you are going to be dealing with money. I hear a lot of the same questions when people talk to me about planning their trip.

How much money should I bring? Should I bring cash? What about debit cards and ATMs? Is there an extra fee for using my credit card?

I’ve been traveling between the US and Mexico for the past eight years, and have learned a lot about travel banking. I have come up with a system to handle my finances that has and continues to save me hundreds of dollars every year. If you’re looking for the best ways to cut fees, prevent fraud, and even invest while traveling, this guide is for you.

How to Get the Best Currency Exchange Rate While Traveling

There are several ways you can change your money for local currency, and each method has a price. But before you try any of the methods listed below, be sure to check the current exchange rate online. The rate you find is the most you can expect to get for your money.

Learn the abbreviation of your home currency and the target currency you’d like to exchange for. When I want to exchange US Dollars for Mexican Pesos, I search the following: $1 USD to MXN.

When you’re ready to convert your money, there are a variety of options. The most common exchange methods are as follows:

Paying With Your National Currency

Some restaurants and convenience stores will allow you to pay US Dollars or Euros. This isn’t very common outside of touristy areas, so don’t expect to see this everywhere you visit. This is one of the worst exchange rates you can get. Generally, a convenience fee of 8-20% built-in when you pay your bill this way. You can do much better than this.

Currency Exchange Kiosks

You’ll find these at airports and in medium to large-sized cities all over the world. Often advertised as “commission-free”, the commission is part of their posted rate. This fee tends to be around 5-8%. Which means you’ll get 5-8% less than the exchange rate you found on Google. This is not a good rate.

Withdrawing Local Currency at ATMs

The rate you’ll get at an ATM is one of the best you’ll find. Usually, this will be within 1% of what you can find online. The biggest downsides to using an ATM are the potential international, bank, and ATM fees. But, if you plan ahead, you can avoid them. Keep reading to find how to avoid these fees.

The Exchange Rate for Credit Cards

Credit cards are great for travel. They can provide consumer protection benefits, primary car rental insurance, and travel rewards. But they will also give you the best exchange rate. I recently did a test to see the rate I was getting with my Chase card, and it was within 0.1% of the posted currency exchange rate on Morningstar. Keep in mind that credit cards are not always accepted throughout Latin America. You’ll have better luck in larger cities.

Also, be aware that American Express and Discover cards are not as widely accepted outside of the US. Just another reason why I use travel-friendly Visa cards.

How to Send Money Abroad

Sometimes travel banking involves sending money to another person or another account abroad. There are dozens of services that offer various ways to do this such as Wells Fargo, but none have been as affordable or reliable as Wise in my experience.

Not only do they offer some of the lowest fees available, but they also offer other useful services for travelers as well. I’m intrigued by their debit card. It gives you free ATM withdrawals up to about $275 USD/mo and allows you to automatically convert your money at the real exchange rate plus a very nominal conversion fee (typically between 0.35% and 1%). If you can’t get the debit card we mention in the next section, this is a fantastic option for international travelers.

However, for travelers heading to Mexico, Colombia, or Argentina, there’s a new player in the field that could offer even more savings—DolarApp. Unlike traditional services, DolarApp allows you to transfer USD into the app for a mere $3 USD fee, converting it into USDC, a stablecoin, at no additional cost. This can then be exchanged into Mexican pesos, Colombian pesos, or Argentine pesos at the current mid-rate without any hidden fees, or you can transfer money directly to other DolarApp users for free. What sets DolarApp apart are its low fees and the convenience it offers travelers in these countries. The platform offers a card that functions like a secured credit or debit card, enabling you to access your funds anywhere cards are accepted. This is particularly beneficial in areas that might not accept international credit cards, ensuring you’re never caught without a way to pay. For those looking to minimize banking fees while traveling in these specific countries, DolarApp presents a compelling alternative worth considering.

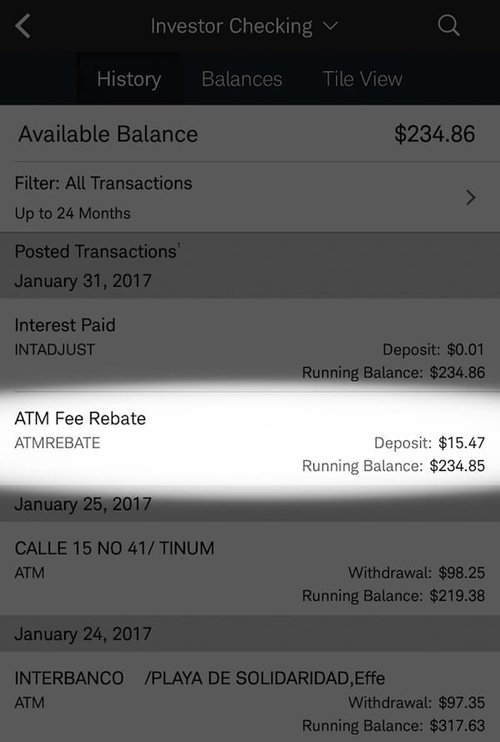

How to Avoid ATM and International Bank Fees

No one likes paying extra for no good reason. Before your trip, make sure you have a debit and credit card that doesn’t charge you unnecessary fees.

For my debit card, I use a Charles Schwab Bank Checking Account. I chose Schwab as my travel checking account for three main reasons:

- No foreign transaction fees

- Unlimited fee rebates from any ATM in the world

- No account maintenance or minimum fees

It’s smart to travel with as little cash as possible, which means visiting the ATM more often. Even if you withdraw cash twice a week, this card will save you hundreds of dollars a year in bank fees. The customer service with Schwab is excellent. At the end of each month, they’ll completely reimburse you for the ATM fees charged to your account.

There was only one thing I thought was strange when I signed up. You have to open a brokerage account with them when you sign up for a checking account, but it turned out to not be a big deal. You don’t have to use the brokerage account if you don’t want to. You’ll still get all the benefits offered by their checking account.

You can apply for this account completely online. There’s no need to visit a physical Charles Schwab branch. They’ll send you a debit card within a week of funding your account.

Another option we mentioned above is the Wise debit card which offers free ATM withdrawals up to $275/mo (they state £200/mo on their website).

Alternatively, if you’re a European reader, I’ve heard that N26 based out of Germany is similar to Schwab when it comes to fees.

For credit cards, I use a Chase Sapphire Reserve or Chase Ink card for business purchases. Both have excellent travel benefits beyond not charging a foreign transaction fee. The Chase Sapphire Preferred is another good option with a much lower annual fee.

Finding the Right Travel Credit Cards

There are dozens of travel credit cards to choose from. The one that’s right for you depends on your spending habits, and how often you travel. As long as you can pay off the balance every month, having a travel credit card can mean much more than free travel.

We’re able to get multiple flights for free every year just by strategically directing our regular spending to the right cards to earn the most points.

Here are the credit cards we use the most:

You read about how to avoid foreign transaction fees and getting the best exchange rate. But did you know that credit cards can help mitigate fraud, and even act as primary car insurance? Some cards will even refund you the application fee for TSA Precheck or Global Entry.

Call Your Bank Before You Travel

Banks are trying to look out for their best interests as well as yours. That’s why most of them have developed sophisticated fraud protection algorithms. This helps make sure the purchases on your card were actually made by you. If your bank thinks you’re in New York, and a transaction suddenly shows up in Mexico City, they’ll block your card. You’ll need to contact them to verify that it was you who tried to make the purchase before using your card again.

Avoid this headache by notifying your bank ahead of time. Let them know where you plan to go and for how long. Some banks allow you to send travel notices online.

How can I keep my credit cards safe while traveling?

Use Multiple Bank accounts

To keep my travel funds safe, I use three banks and three accounts:

- General Savings Account,

- Personal Checking Account,

- Travel Checking Account.

Why three? Let me explain.

It doesn’t make sense to have the bulk of my savings sitting in a checking account gaining hardly any interest. I use Wealthfront for my savings where I get a 5% interest rate, more than ten times what I’d get in a regular checking account. Also, having my savings separate from other banks allows me to keep it safer. I don’t travel with a card for this bank.

I use my personal checking account to pay my bills, and make transfers to my other accounts. For safety, I keep less than what I have in my savings in this account, but more than what’s in my travel checking. Since I don’t carry a debit card for this account while traveling, there’s less risk of fraud.

My travel account is only tied to one other account to make electronic transfers quick and easy. This also protects the other remaining account. I never keep more than $600 in my travel checking account. Even in the unlikely event that I am forced to withdraw all the money in it, it wouldn’t mean the end of my travels.

Emergency Cash Stash

In case I ever find myself in a situation where I am unable to access my bank card or an ATM, I still keep some cash with me. A two week emergency stash gives me peace of mind. Two weeks should be plenty of time to get somewhere with an ATM, or have the bank mail out replacement cards. For traveling through Mexico, I like to keep an extra $300 USD set aside.

For extra safety, some of my travel shirts have a secret pocket sewn into them where I can stash my emergency fund. These also happen to be my favorite shirts to wear anyway as they’re made out of a simple yet comfortable hemp and cotton blend. You can get them here.

Use a Dummy Wallet

In particularly dangerous areas I carry a dummy wallet. This is the wallet I would hypothetically reach for if I were mugged. Thankfully that hasn’t happened. But if it were to happen, hopefully a mugger wouldn’t get away with much. I tend to keep $10-20 in my dummy wallet, along with a couple of expired credit cards. I keep it in my back pocket and my main wallet elsewhere. While there’s no knowing what could happen in a dangerous situation with a mugger, I would theoretically first throw them this wallet, then run the other direction. Optimistically that would placate their need for more of my things while I make a speedy getaway.

Understanding Dynamic Currency Conversion

“Would you like to be charged in dollars or pesos?”

When traveling, you might be asked whether you want to pay in local currency (pesos in Mexico) or your home currency (dollars, for example). This practice, known as Dynamic Currency Conversion (DCC), offers convenience but can come with a less favorable exchange rate.

For instance, while purchasing tickets at Xel-Ha in the Riviera Maya, I was offered the option to pay in pesos or dollars. This choice might seem trivial, but it can impact how much you’re charged due to varying exchange rates.

The underlying principle: When you opt to pay in your home currency, the vendor converts the price at their rate, which may not be as competitive as your bank’s rate. Normally, your bank automatically converts international transactions to your home currency, often at a more favorable rate.

The proactive approach: To ensure the best exchange rate, it’s advisable to always choose to be charged in the local currency.

If you’re inadvertently charged in your home currency, you can contact your bank. If you have a travel-friendly card without foreign transaction fees, inform your bank of the charge amount. They can usually refund the difference based on the interbank exchange rate at the transaction time. This process is generally straightforward and can be completed over the phone in about five minutes. While there’s no need to confront the vendor, informing them of your preference for local currency billing in future transactions can be helpful.

Digital Security While Traveling

Online Security 101:

Ensuring the security of your personal information is paramount, especially while traveling. For this, create a unique password for every online account you have. Passwords should be lengthy and difficult to guess, and should never be shared with anyone. While this may seem cumbersome, password managers like Bitwarden make it easy.

Store all your essential information such as passport and banking details in a secure digital vault like Bitwarden. In case of an emergency, this will facilitate quick contact with your bank or reporting a stolen passport. Don’t forget to turn on multi-factor authentication on all your accounts for enhanced security.

Additionally, having a separate email address that you share only with your bank or other entities with which you share sensitive information is a wise move. This can go a long way in preventing account takeovers and identity theft. For this purpose, we recommend Proton Mail, which prioritizes your privacy and provides end-to-end encrypted and password-protected emails for added safety and privacy.

Use a VPN

While traveling, it’s important to safeguard your personal information by using a reliable Virtual Private Network (VPN). We recommend Proton VPN, a service provided by the same Swiss-based company that offers Proton Mail, to encrypt your personal data while browsing the internet. It’s prudent to treat all open Wi-Fi networks as potential security risks, and using a VPN like Proton VPN can help secure your online activities from prying eyes. For further insight into the importance of VPNs and their benefits, you can check out a comprehensive guide here.

Related:

Investing While Traveling Abroad

Assuming you’ve read this far, congratulations. You are part of a small fraction of the world that has it so good you can entertain the idea of traveling the world. For those of you who can travel the world and have money left over, I recommend using Wealthfront.

I’ve been an entrepreneur for over a decade now, and I waited too long to learn about investing. There are swaths of books written on the subject, but I’d rather focus my time on what I’m passionate about. That’s why I use Wealthfront, which has made investing super easy. They use proprietary algorithms to invest your money based on your adversity to risk. Use this link, you’ll get your first $5,000 managed for free.

PREPARING FOR A TRIP TO MEXICO? NEED TO CONVERT YOUR US DOLLARS TO PESOS? DO YOU KNOW THE BEST WAY TO GET GREAT EXCHANGE RATE? WE ANSWER ALL THAT AND MORE ON THIS SPECIAL FEATURE ALL ABOUT MEXICAN MONEY.

Conclusion

Life is too short to learn all the lessons the hard way. I hope this guide saves you hundreds of dollars extends your travels. Let me know if I missed anything in the comments. What is your favorite travel card? Have you used any of the services mentioned in this post before? What was your experience with them?

Related Posts

How to Visit the Bioluminescent Bay in Mosquito Bay in Vieques, Puerto Rico

The 16 Best Things to Do in Barcelona

Spanish Immersion Retreat in Guanajuato: A Personal Experience